Academic Frontier

Academic Frontier

Nanocellulose: market prospects

QQ Academic Group: 1092348845

Detailed

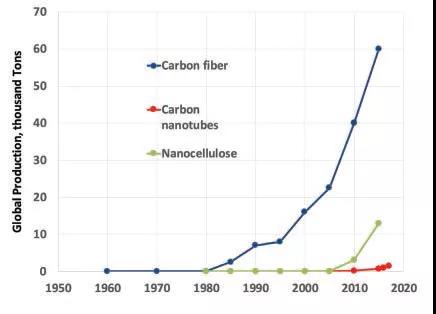

Nanocellulose is derived from cheap and abundant biological materials, with high strength, light weight, non-toxicity, and lower cost than other nanomaterials. So why didn‘t this industry develop faster? In fact, it takes a long time for new advanced materials to appear. For example, plastics have existed for more than 50 years before they were widely accepted. Among the latest advanced materials, carbon fiber was invented around 1960, and has not exceeded 10,000 tons in the past 40 years. Nanocellulose is also on a similar track (see figure below). Nanocellulose has made great progress so far, but whether it is technical or commercial, the challenges remain.

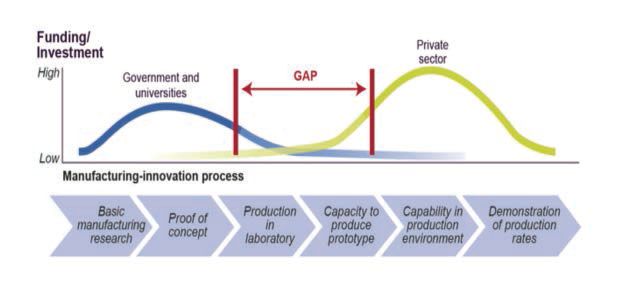

The chart below depicts the investment gap, also known as Death Valley, because this is where startups often die. This chart simply tells the story of the development of the nanocellulose market.

There are four key pieces of information about the investment gap chart:

1. This chart is not drawn to scale. The investment required for the complete commercialization of a private enterprise is much larger than that depicted in the chart.

2. The capital for this investment must ultimately come from customers, and must come from a reasonable value proposition.

3. The industry is effectively bridging this gap. What is more encouraging is that no new nanocellulose company is currently dying in Death Valley.

4. However, the main funds from customers are still not available for development, and companies often obtain funds from equity partners.

After research, the construction of a 50-ton/day CNC production plant requires a capital investment of up to US$180 million, depending on the plant’s construction site and whether sulfuric acid is recovered. In addition to cost issues and typical technical challenges such as compatibility and drying/redistribution, there are commercial challenges that hinder customer support. Among these challenges, the most important is the need to assert its development value throughout the supply chain. Although some commercial applications have been reported, such as oil and gas drilling fluids, adult diapers, coatings, composite materials, latex, cosmetics, gel ink for pens, and gel for running shoes. However, these companies have not yet developed to the point where they can generate sufficient revenue to finance commercial-scale investments, so the industry is still largely in the investment gap.

The good news is that the industry is steadily crossing the gap and finding funding where needed. With the exception of one or two paper mills that were closed due to paper industry conditions, no company that entered the field of nanocellulose production exited. However, the challenges of business development remain, because most of the funds come from equity partners, not customers:

• Celluforce: In addition to initial funds from Domtar and FPInnovations, it also received equity investments from Schlumberger and Fibria (now Suzano).

• American Process: Acquired by Granbio.

• FiberLean: Jointly established by Omya and Imerys.

• Melodea: It is an equity investment from Klabin and Holmen.

Market outlook

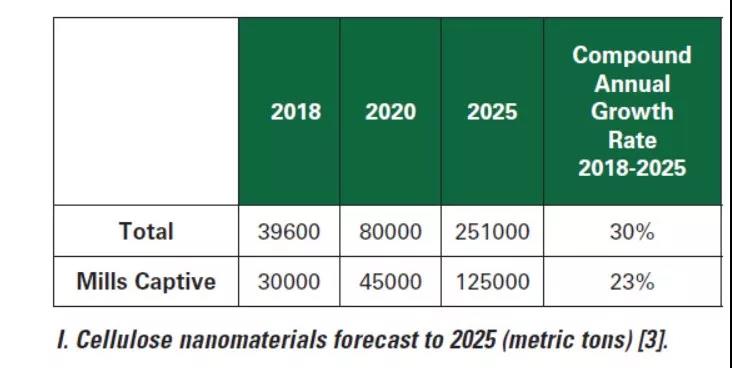

For factories that produce microfibrillated cellulose (MFC) and use it for their own paper and paperboard, this material does not need to be dried before being added to the paper machine, nor does it need to be transported over long distances, which greatly reduces costs. In fact, in 2019, a bio-based market research on nano-cellulose for packaging showed that more than 75% of nano-cellulose was produced in factories in 2018 and used in its own products on site. Most of them are unreported, but we do know the work of some companies, such as Stora Enso, Norske Skog, BillerudKorsnäs and International Paper, as well as some instructions from FiberLean. In the market research in 2019, the bio-based market estimated that the output of nanocellulose in 2018 was about 40,000 metric tons, which is expected to grow at a rate of 30% per year (see the table below).

Although most paper and cardboard mills produce nanocellulose, or microfibrillated cellulose (MFC), and use it for their own products, other applications are beginning to grow rapidly and close the gap. The largest output is FiberLean‘s MFC mineral composite material, with 8800 tons of MFC used in three paper and board mills worldwide and a demonstration plant in the United Kingdom. This is followed by Kruger, which has 6,000 tons of nanofibrillated cellulose (CNF) used in the company’s own paper and paperboard, among other uses. The biggest seller of nanocellulose is probably Borregaard with 1,100 tons, but this is still on a demonstration scale.

Leading manufacturers are working on cooperation, joint development agreements, and even supply agreements. In Europe and Asia, dozens of alliances have been established, some of which include several levels of the supply chain, from producers to end users plus intermediaries. In Japan, the Nanocellulose Forum is an alliance of 220 companies, including Japan Paper, Oji Holdings, Toyota Motor, Mitsubishi Motors, Mitsui Chemicals, etc. In Europe, the Bio-Industrial Joint Venture (BBI JU) is a public-private partnership between the European Union and the Bio-Industry Alliance. It invested 3.7 billion euros in 2014-2020, of which Horizon invested 975 million euros in 2020 and private investment 2.7 billion euros. In the United States, the Pulp and Paper Technology Innovation Alliance (APPTI) is also exploring opportunities for joint research in the areas of composite compatibility, drying/dehydration, and redispersion. It was suggested that middlemen and end users also participate. This joint effort will advance the development of technology and help manufacturers understand the needs of customers in depth.

Jack Miller,

Biobased Markets

For full text see: Jack Miller, Nanocellulose: Market perspectives, TAPPI JOURNAL, 2019, VOL. 18 NO. 5:313-316.

Source of information: Linda Nano

This information originates from the Internet for academic exchange only. If there is infringement, please contact us to delete

The chart below depicts the investment gap, also known as Death Valley, because this is where startups often die. This chart simply tells the story of the development of the nanocellulose market.

There are four key pieces of information about the investment gap chart:

1. This chart is not drawn to scale. The investment required for the complete commercialization of a private enterprise is much larger than that depicted in the chart.

2. The capital for this investment must ultimately come from customers, and must come from a reasonable value proposition.

3. The industry is effectively bridging this gap. What is more encouraging is that no new nanocellulose company is currently dying in Death Valley.

4. However, the main funds from customers are still not available for development, and companies often obtain funds from equity partners.

After research, the construction of a 50-ton/day CNC production plant requires a capital investment of up to US$180 million, depending on the plant’s construction site and whether sulfuric acid is recovered. In addition to cost issues and typical technical challenges such as compatibility and drying/redistribution, there are commercial challenges that hinder customer support. Among these challenges, the most important is the need to assert its development value throughout the supply chain. Although some commercial applications have been reported, such as oil and gas drilling fluids, adult diapers, coatings, composite materials, latex, cosmetics, gel ink for pens, and gel for running shoes. However, these companies have not yet developed to the point where they can generate sufficient revenue to finance commercial-scale investments, so the industry is still largely in the investment gap.

The good news is that the industry is steadily crossing the gap and finding funding where needed. With the exception of one or two paper mills that were closed due to paper industry conditions, no company that entered the field of nanocellulose production exited. However, the challenges of business development remain, because most of the funds come from equity partners, not customers:

• Celluforce: In addition to initial funds from Domtar and FPInnovations, it also received equity investments from Schlumberger and Fibria (now Suzano).

• American Process: Acquired by Granbio.

• FiberLean: Jointly established by Omya and Imerys.

• Melodea: It is an equity investment from Klabin and Holmen.

Market outlook

For factories that produce microfibrillated cellulose (MFC) and use it for their own paper and paperboard, this material does not need to be dried before being added to the paper machine, nor does it need to be transported over long distances, which greatly reduces costs. In fact, in 2019, a bio-based market research on nano-cellulose for packaging showed that more than 75% of nano-cellulose was produced in factories in 2018 and used in its own products on site. Most of them are unreported, but we do know the work of some companies, such as Stora Enso, Norske Skog, BillerudKorsnäs and International Paper, as well as some instructions from FiberLean. In the market research in 2019, the bio-based market estimated that the output of nanocellulose in 2018 was about 40,000 metric tons, which is expected to grow at a rate of 30% per year (see the table below).

Although most paper and cardboard mills produce nanocellulose, or microfibrillated cellulose (MFC), and use it for their own products, other applications are beginning to grow rapidly and close the gap. The largest output is FiberLean‘s MFC mineral composite material, with 8800 tons of MFC used in three paper and board mills worldwide and a demonstration plant in the United Kingdom. This is followed by Kruger, which has 6,000 tons of nanofibrillated cellulose (CNF) used in the company’s own paper and paperboard, among other uses. The biggest seller of nanocellulose is probably Borregaard with 1,100 tons, but this is still on a demonstration scale.

Leading manufacturers are working on cooperation, joint development agreements, and even supply agreements. In Europe and Asia, dozens of alliances have been established, some of which include several levels of the supply chain, from producers to end users plus intermediaries. In Japan, the Nanocellulose Forum is an alliance of 220 companies, including Japan Paper, Oji Holdings, Toyota Motor, Mitsubishi Motors, Mitsui Chemicals, etc. In Europe, the Bio-Industrial Joint Venture (BBI JU) is a public-private partnership between the European Union and the Bio-Industry Alliance. It invested 3.7 billion euros in 2014-2020, of which Horizon invested 975 million euros in 2020 and private investment 2.7 billion euros. In the United States, the Pulp and Paper Technology Innovation Alliance (APPTI) is also exploring opportunities for joint research in the areas of composite compatibility, drying/dehydration, and redispersion. It was suggested that middlemen and end users also participate. This joint effort will advance the development of technology and help manufacturers understand the needs of customers in depth.

Jack Miller,

Biobased Markets

For full text see: Jack Miller, Nanocellulose: Market perspectives, TAPPI JOURNAL, 2019, VOL. 18 NO. 5:313-316.

Source of information: Linda Nano

This information originates from the Internet for academic exchange only. If there is infringement, please contact us to delete

- Previous: Carbon dot hydrogel AS

- Next: Bioactive Materials |